The Short Term Profits Industry- Cement

- Apr 23, 2019

- 5 min read

The Ministry of Commerce & Industry publishes the Index of Industrial Production, popularly known as the IIP, every month, as it is a leading indicator of things to come in the economy. Eight sectors in the IIP constitute nearly 40.27% of it, making them quintessential parts of the modernized industrial economy of India.

These are quintessential not only because of the fact that they churn the mechanized industrial machine but also because of the fact that they employ a substantial portion of the country.

These eight sectors are:

Coal

Crude Oil

Natural gas

Refinery Products

Fertilizers

Steel

Cement

Electricity

You can find the link to the Government’s document here.

So, when there are eight indefatigable industries powering the nation, why should we turn our gaze to the cement sector only?

Because the index that the Government published on the growth in each of these sectors shows that momentous growth has taken place on the leading indicator side of the cement industry. To support the same, consider the following index growth rate table published by the Ministry of Commerce and Industry:

It is evident that the 13.6% growth in the cement industry skews the IIP. And being an IIP starved nation, the market will welcome the same as a breath of fresh air. The over-arching growth in the cement industry will then manifest itself as the reaper of the largest harvest- dividends and price appreciation.

It is with this premise that we begin our fundamental analysis of the cement industry.

Now, what are the forces that have actually bolstered this tremendous growth in the cement industry?

At the forefront of it is the sheer size of the industry. It cannot be forgotten that India is the second largest producer and consumer of cement across the globe. This means that a ready market is available to pay for its consumption needs. Add to this massive market size the fact that this sector has a high level of correlation with the construction industry, which is the second largest employer of the population after the agriculture and allied services industry, and you soon figure out that cement as a product is “too big to fail.” This provides cautious investors protection, that is seldom afforded by the market.

The Indian cement industry has more than 400 plants, 210 of which account for nearly 80% of all annual cement production. Moreover, the top 40 companies in the sector cater to nearly 90% of the demand.

Secondly, there is the election fever. Every time the parliament goes about to fill its seats, the easiest way they find to commit to the people their services is by offering infrastructure. We are an infrastructurally developing nation, and there is room for a tremendous amount of improvement. The Government finds the mobilization of cement, sand, rock and labour the most economical way to get the growth engine churning before every election. The same is the story with this year’s momentum.

The Government has committed itself to many infrastructural growth stories like housing for all by 2022, the dedicated freight corridor, smart cities, high-speed railways, road, bridges, dams, etc.

All this has provided a major impetus to the demand for cement and the growth in the cement industry.

Next, there has been an improvement in the impediments of FY2018, that has resulted in better efficiency in the cement industry- like higher axle loading, removal of the ban on the pet coke utilization in cement kiln located in Northern India, volatile crude prices, etc.

It is to be noted that there is a regional concentration in the cement industry. There are two specific reasons for the same. Firstly, limestone reserves are majorly located in belts across Rajasthan in the North, Madhya Pradesh in the Centre and West, and Andhra Pradesh in the South. And secondly, the low shelf life of cement. The cement hardens and solidifies into a mass of rock if kept in contact with air for a decent amount of time. Due to these reasons, cement is procured, produced and supplied locally across India, dividing the market into North, East, West South and Central.

And finally, the cyclicality of the cement industry. The fourth quarter is always the best quarter for the construction industry. Most construction activities are slow during the summers and monsoons, with major activity picking up after Diwali. All management calls have given the investors a positive outlook for demand during Q4-FY2019, and the Government’s focus on the infrastructural growth story has not been shaken. The same can be expected to hold good, at least till the monsoon session of the parliament. The future of the same though is dependent on the incoming Government.

So, now that we are convinced about the wealth generation capacity of the cement industry in the near future, we may ask the question as to which stock deserves the warmth of your money?

The first criteria to select the stock is to have all the following three ticked by the company:

Strong backward integration of operations- Limestone mines, coal linkages, captive power sources

Large distribution network

Pricing power

So which stock to buy?

I have shortlisted six stock based on their market capitalization, the price of an individual piece of stock (so that an ordinary individual investor can buy the share) and availability of public information.

In the following list of comparative analysis, we see that Ultratech Cement is highly overvalued (and rightly so considering the sheer production capacity of the company), Ambuja, JK Cement and ACC are slightly undervalued, while Heidelberg and Ramco are slightly overvalued.

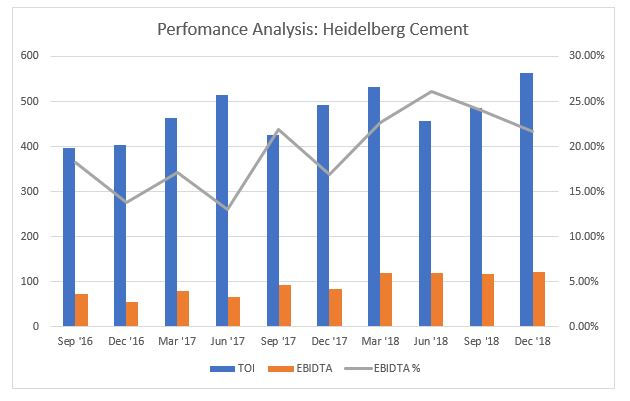

The following graphs plot the quarterly performance of each of these companies, and we see a trend where most of the large players have stabilizing margins.

Ramco has shrinking margins, while Heidelberg has a moderate upward trend in margins.

All these 6 stocks are good stocks and will earn you money when the results come out. They are among the top 10 players in the industry with considerable pedigree backing them up. However, I wish to go an extra arm’s length and suggest Heidelberg.

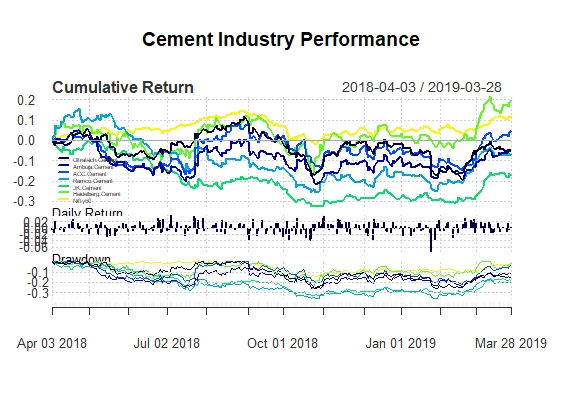

It is already visible that the margin of Heidelberg is showing an upward trend. Now, once we plot the performance of all these stocks against the benchmark- Nifty, the reason to hold Heidelberg for the short term becomes even stronger.

It is the only stock to have outperformed the Nifty during FY2018. This is because of the fact that the market expects this company to perform. The company belongs to Heidelberg AG of Germany, which has a global footprint in the cement market, and a sufficiently strong balance sheet.

Now you might say that the slight overvaluation in PE shows that the market knows there is higher certainty in Heidelberg to reach the estimated performance, and thus the market is willing to pay a slight premium to own the stock. The market has also discounted the above fact to help it beat the Nifty. But what makes Heidelberg a great choice is the fact that while Ramco is twice the size of Heidelberg, the stock commands the same certainty premium in PE. This means that when the company reaches the estimated performance, the smaller size of the company will compel the management to explore expansion, which is when the stock will gain further price appreciation and momentum. The present momentum will also be bolstered by a good Q4 result, which will, in turn, help you book the short-term profit.

But the extra protection, that Heidelberg provides in the smaller size of the company, will help you make a safe return in the future in case the present performance falters, which in my opinion is highly unlikely.

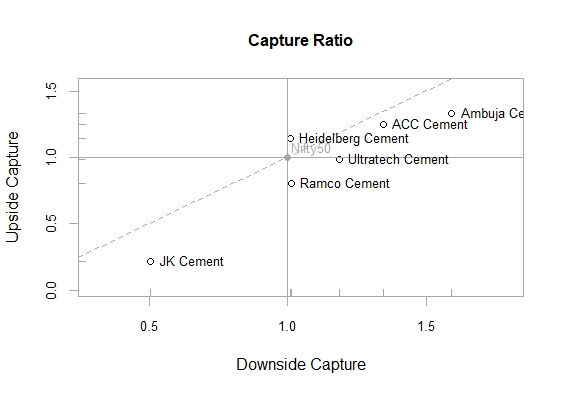

This is evident from the following plot of the capture ratios which shows that Heidelberg is the only stock among its peers to have a higher upside bias compared to a downside bias. Considering the rising Nifty and Sensex, the market forces itself pose to be a great force to help Heidelberg deliver the short-term profits you seek.

And with that, we come to an end to this discussion. I hope that this analysis will help you gain better clarity of the industry and add value to your portfolio creation.

Happy investing!

P.S.- All analysis is based on publicly available information.

Comments