Stock Picks: Q1-FY2020

- May 5, 2019

- 6 min read

Hello! Welcome to Insignia Investments. My name is Roop Pratim Datta and today I am going to discuss with you three stocks and why I think they deserve your money and your attention.

Before we jump start with the recommendations, I will reiterate my investment philosophy and objective. I work hard to earn money. So, I am not willing to gamble it to make fabulous returns or losses, whichever hits first, but rather I am always on the lookout for market return or better. I am happy with a modest return that the market is willing to provide or better if my calculations are on spot. I do not enjoy market upheavals and my objective for investing is to save for my retirement.

Now that we are clear on the investment philosophy, let's discuss my screening methodology. As I have said earlier, I go for the industry first, and then follow it up with the individual company’s business model, then its financials and finally the management. My education helps me be conversant with macro-economics, and I try and use that resource to the best of my ability to look for signals ahead of time.

And finally, the disclaimer. I am just an ordinary individual investor like you and do not have any proprietary software like Bloomberg or any other subscription to help my analysis. All the data I share with you here be found in the public domain.

Let’s begin.

The first stock that grabbed my attention was Gujarat Fluorochemicals Limited. The chemicals sector has been minting money of the last year, and business results across the spectrum have been good. The thing that makes this stock attractive is its strong core business model in the fluorochemicals sector, adequately stable and diversified subsidiaries and JV and a healthy financial statement.

Gujarat Fluorochemicals Limited (GFL) is the flagship company of the Inox Group, which also holds the more famous Inox multiplexes, and is the largest polytetrafluoroethylene (PTFE), chloromethanes and refrigerant manufacturer in India, and among the top 4 globally.

The group also has interests in wind power generation, industrial gasses and cryogenic storage.

More than 50% of the group’s revenue comes from GFL, and the company has adequate backward integration, providing much comfort to the operating margins.

The comfort in the company is drawn from the rising margins, the economies of scale, the backward integration and the diversified product portfolio consisting of specialty products. The company has a low gearing of 0.34 times and had ₹ 680 crores of liquidity in the balance sheet at March 31, 2018.

The current market price of the stock is ₹ 1048.45. The PE ratio of the company is 45.84 times against the industry benchmark of 23.88. The PB ratio of the company is 2.43 against the industry benchmark of 2.36. This suggests over-valuation, but the same is justified considering the strength in the business model and the strong financials with low leverage. This gives the company adequate headroom to expand operations and pursue capex if required.

Kindly refer to these graphs for understanding the historical performance of the stock for the last year.

The strong quarter on quarter movement and the stable margin makes this stock very attractive.

I ran the following charts on R- a statistical analysis software to compare it against its peers. Have a look:

The capture ratio shows that stock is defensive with market uptick being favoured over market downturns.

Plotting the annualized returns against the annualized risk shows that the stock has had an attractive profile, much akin to Pidilite, over the last one year.

Considering the robustness of the business model, the size and the strong financial position, and combine the same with the historical performance of the company, Gujarat Fluorochemicals looks like an attractive package at a just price.

There are only two major risk components to keep an eye out for when you hold this stock. They are government regulations in the industry and the working capital intensity in the company. Given the strong financials and the size of the company, it is most likely to weather such risks for the short term, but any long term negative changes in the industry can affect this stock’s valuation adversely.

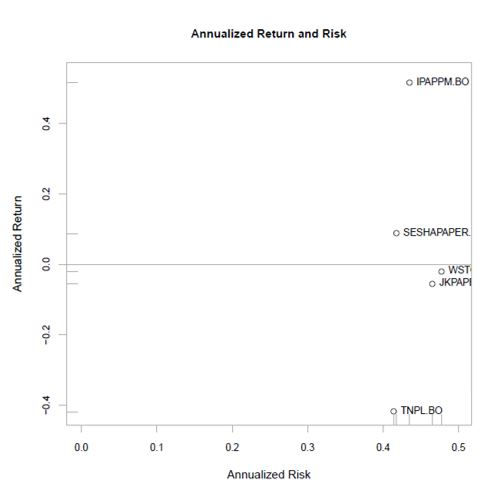

The second stock that I find having wealth creation capacity in the medium term is JK Papers. The ban on the import of certain grades of waste paper by China during the last year has resulted in a drastic rise in the price of wood pulp. This, in turn, has resulted in the lower production of certain grades of paper by China, and the world had to turn to India to fill up the vacuum. However, the dynamics do does not end there. The increased pulp prices forced the non-integrated players to bite the dust, and the players with integrated farmlands and cultivation to enjoy a comparative boost in the margin.

Add to this the fact that the industry has had nearly no significant capacity expansion other than that of JK Paper, and you start seeing why JK paper is one of the better companies to invest in the paper segment.

Paper industry is in the upward swing modem, and with the enhanced capacity, nearly 100% capacity utilization and the incremental market share, JK Paper is poised to rake in serious amounts of operational growth and valuation appreciation.

Consider the Q-o-Q performance of the company, shown in the following graph:

The company’s management has been quick to realize the cash accruals into quicker deleveraging, from 1.29 times on March 31, 2017, to 0.80 times on March 31, 2018.

Looking at the historical performance of the stock, we see the following:

The stock is very well poised to recover from the earlier positions of being marginally extra sensitive to market downturns than market upticks.

The PE ratio of the stock is 10.45 against an industry benchmark of 23.88. The PB ratio of the stock is 1.63 against an industry benchmark of 2.36. In terms of relative valuation, the stock is available at a discount. The current market price of the stock is ₹ 143.80.

The key monitorable however remain the Chinese influence, in addition to the market cyclicality and leverage.

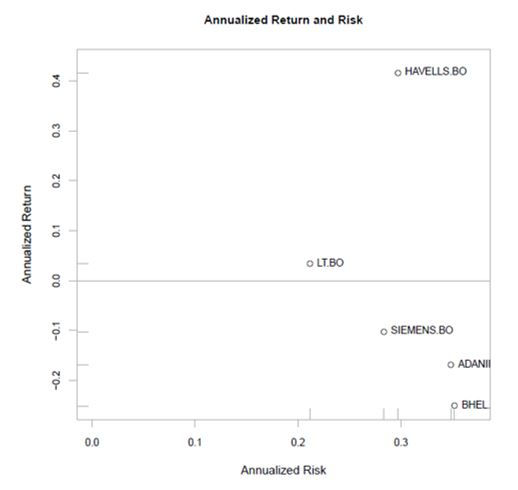

The analysis of the final sock tells me that it is a pricey consistent performer. Wile the valuation of the stock makes me a little conservative about the stock, but the operational efficiency, expertise and the ability to not be quickly replaced by any run-of-the-mill company make this a long term stay for the steady appreciation of the holding. My final stock of choice is Siemens Ltd.

I am a little biased towards the engineering sector because it takes years to build expertise, cannot be easily shaken by new entrants and is less likely to be ousted in a growing economy like India where the IIP is only going to move up in the long-term scenario.

Siemens Limited is a company that is at the juncture of a turn around as we speak. The company is surely exposed to slow grinding sectors like power and transmission, but the management has realized the same and has made effective transitions in the digital and automation realm.

I do agree that the merger of Alstom and Siemens AG (Germany) would have made the valuation go through the roof, but even now the company is a confident key player in the electrical and electronics engineering segment, with a massive market capitalization.

What attracts me to this stock are:

Geographically distributed clientele

Diversified business portfolio

Established track record

Parent support

Zero debt in the books

This company is not going to die at any rate. The most that can happen is that it raises debt to undertake the business transformation. However, do note that this stock is going to be a bedrock stock and not your rise quickly and exit the stock. My investment-call on this stock is based on the strong financial position of the company and the long years of engineering excellence it packs.

For your reference:

And with that, we come to the end of this video. I hope that this discussion adds value to your portfolio selection. And, as I always say, do not go by my words, but rather used this as a reference and do your own analysis and see if you come to the same conviction for the stocks I have discussed. If you do, I would love to head about it in the comments section down below. I would also love to hear the things you would like me to discuss in future blogs.

You can also reach out to me at insigniainvestments@gmail.com.

Happy investing!

Comments